The House/Fab Always Wins

Lawrence Lundy’s State of the Future: Dispatch from 19 June 2026

Welcome, Ladies and Gentlemen, to the 8th wonder of the world, the flow of the century, always timeless, thanks for opening this, you could have been anywhere in the world, but you’re here with me, I appreciate that. Uh.

I just can’t open Claude Code today. I just can’t do it. Do we have a word for Claude overload yet? Like email overload. Zero inbox just isn’t achievable. Sooo many agents, so many tasks. Turns out the locks on my back door void my home insurance. Who knew. And turns out Shin-Etsu is already worth $86bn with 22.6 Fwd P/E and PEG of 2.1. and is the cleanest buy for the litho-resist category. But what about TOK, or Fujifilm? Run the stock analysis skill. And how is my health paper tracking coming along? A Oral PCSK9 — enlicitide (MK-0616) in Phase 3, ~50-60% LDL reduction. It’s the convenient pill version of the potent injectable PCSK9 drugs. I see. Great. What do I do with that. And what did the tiler say about the quote for the London Mosaic heritage encaustic tiles for the hallway? Draft a chase. Ahhhhhhhh. It’s f*cking 4pm. I haven’t moved.

Is this life now?

[Well, it’s life for about 1 more generation until all these tasks are autonomous loops]

Is it Jevon’s paradox up until it isn’t? 1 more gen and it really is keynes economic possibilities for our grandchildren.

But for now, folks, it’s just agent switching until we all go mad.

Here is a long one but a good one. I spent last week on holiday, writing and clauding, and writing and clauding. Behold:

Apple? Anyone?

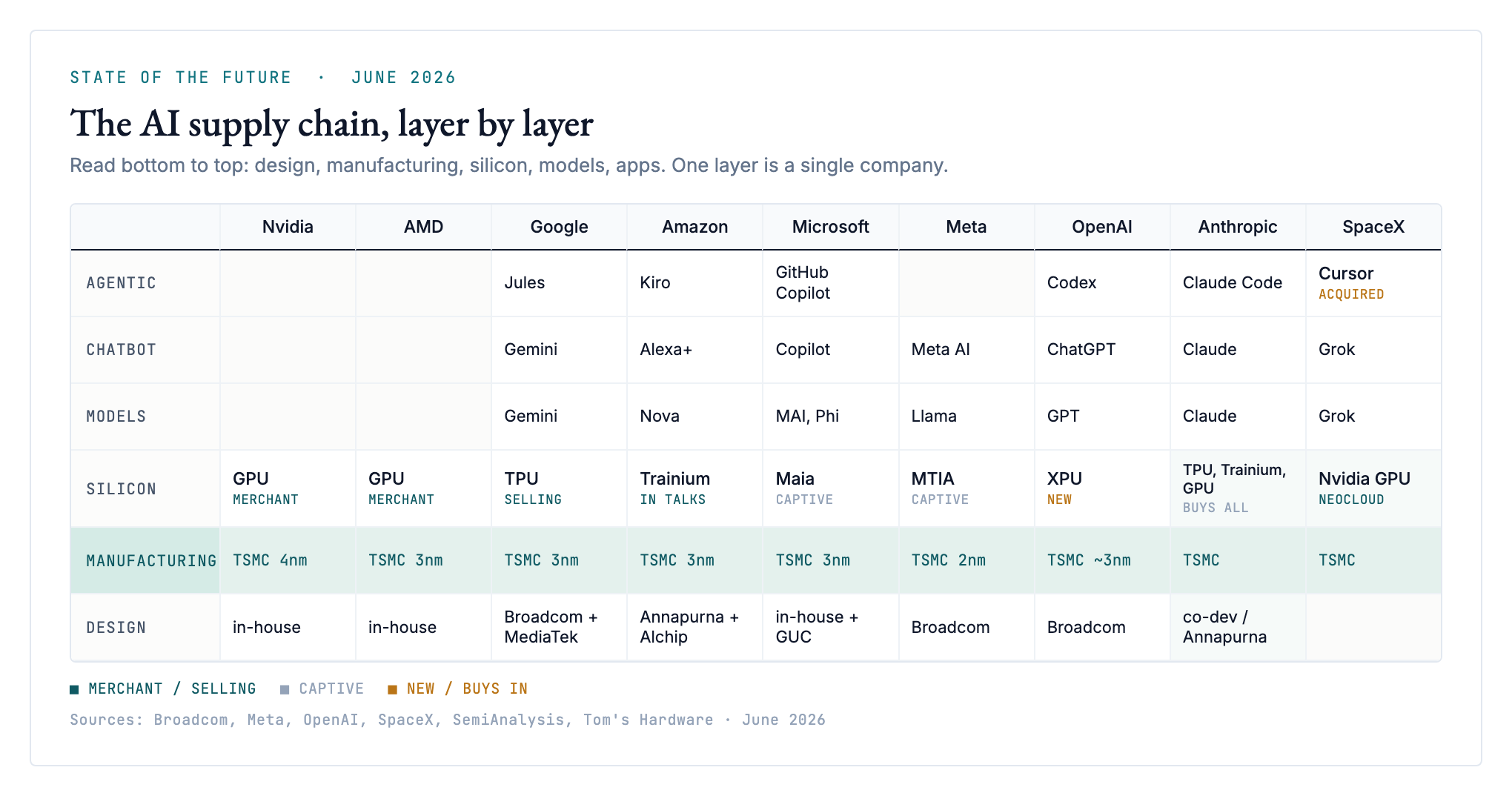

The pattern is that everyone is moving into everyone else’s layer. Bunfight they call it. Or bumfight. I don’t know which. And I’m not gonna find out either. You will be able to tell proof-of-humanhood soon by just spotting a mistape.

The model labs are designing their own chips now. OpenAI is building a 10GW accelerator with Broadcom. Anthropic co-develops Trainium with Amazon.

The hyperscalers that built chips for themselves are turning around and selling them, Google to outside data centres, Amazon the same.

Nvidia, which only ever sold the chip, is buying equity in the labs that buy the chip.

And Intel, the one firm in the picture that was a chip vendor first, is moving in the opposite direction, down into the fab. It is a value chain eating itself.

But look at manufacturing: TSMC, TSMC, TSMC, all the way across, nine companies, one manufacturer.

Fabs were once the worst business in semis.

The base is sold out, and it is putting up prices

I wrote a version of this back in December, in LFG (for semiconductors): the foundry layer is where the next decade of value capture lives. The numbers since then have made the case stronger. TSMC’s 2nm node is sold out for 2026, with customers appling for allocation out to mid-2027. Its advanced packaging, the CoWoS step that bolts the logic to the memory, is booked through 2027 on lead times of a year or more. Plus, it’s raising prices into that demand, 3nm wafers up about 15% in H2, packaging prices climbing 10-20% a year against 5% for ordinary logic. TSMC has lifted its long-run gross-margin floor from 53% to 56% apparently in the middle of the biggest capital build in its history. Demand is strong. Monopoly pricing.

The same is true one shelf over, in memory. High-bandwidth memory (HBM) is sold out industry-wide, with buyers receiving barely 1/2 or 2/3 of what they ask for, and contract prices look set to roughly double into 2027. And upstream of all of it sits ASML, the lithography monopoly, the single chokepoint the whole industry’s constraint is migrating towards. 2029, you just wait.

The bull case for the layer above is real. Nvidia is not losing this. Its data-centre business did $75bn last quarter at a 75% gross margin, and the share it cedes to custom chips over the next year is more like 10 points than 50. The thing eroding Nvidia is the hyperscalers’ own silicon, not AMD, but that erosion is slow. I said it in The Compute Gradient and I’ll say it again: the competitors are breaking Nvidia’s monopoly, not its moat. Those are different things.

But see what happens to the value even when a hyperscaler “wins.” When Google sells you a TPU, Broadcom took a design fee, TSMC took the wafer, and the memory came from 1 of 3 Korean and American firms. Google keeps a cloud margin. The chip designers fight over the scraps in the middle. The design layer is a real market with real winners and losers, which is exactly why it is not where the durable money sits. See memory wars. The money runs through it, down to the fab. Not a moat. What‘s the opposite of a moat? A sieve? Sounds right.

The surprise upstairs: the model isn’t commoditising

Here is where my own prior was wrong. The consensus line, mine included, was that raw model capability commoditises, prices race to zero, and the value flees upward to the application or downward to the chip. Half of that is happening. At a fixed level of quality, the price of a token really is falling about 10x a year, which is astonishing and deflationary and exactly what you’d expect.

And yet the frontier labs are putting their prices up. GPT-5.5 launched at double its predecessor. Anthropic’s inference gross margins went from the high thirties to over 70% in a year. I don’t even want to know what I will have to pay for Fable if I can get my hands on it. The reason is agents. An agentic task burns 5 to 30x the tokens of a chat, because it re-reads its whole context at every step, and that wall of demand has been raising the clearing price of a frontier token faster than the cost of serving one has fallen. So the model layer keeps its pricing power as long as it stays ahead, and the margin pain has moved somewhere else entirely, downstream, to the application layer, where gross margins have slid from the 80s into the 50s as the cost of the underlying intelligence eats the SaaS economics alive.

You can watch it happen in agentic coding. Cursor was doing 2.5bn dollars of ARR and just got bought by SpaceX for 60bn. Claude Code is on a similar run-rate, Codex has 4 million weekly developers. Extraordinary growth, and yet the standalone tools keep getting absorbed, Cursor into SpaceX, Windsurf into Cognition, because the in-editor assistant is commoditising back towards whoever owns the model. The durable winners up here look like the labs’ own agents and the odd wedge into people who can’t code at all. Maybe old industry consulting. But the labs are making a play there too. Everyone else is just renting their moat from the layer below. Can you rent a moat?

What changed? The constraint moved twice

If you only take two things from this, take these.

Uno, is that the binding physical constraint is no longer chips. It is power. Satya said the quiet part out loud, that Microsoft has chips sitting in inventory it can’t plug in because it doesn’t have the “warm shells,” the buildings with power, to put them in. Jensen calls AI “a power-limited industry.” American data-centre demand goes from 31GW last year to 66GW by 2027. Gas turbines are sold out to the end of the decade, big transformers run 2-4 years out + grid-connection queues stretch past 5. The American energy department issued an emergency order last month letting the grid operator switch data centres off when the system is stressed. None of that gets fixed inside a year. Power is the new toll booth, and the market I don’t think has started to price it. Diligence pending.

Deux, is that the risk is no longer demand. It’s money. The 4 big clouds will spend something like a trillion dollars this year. Data-centre construction is already a large chunk of US GDP growth. And it’s not really cash flow anymore, it’s debt and a tangle of circular financing, Nvidia into OpenAI into Oracle into AMD into CoreWeave, that even Jensen calls “ridiculous” while doing it. The Federal Reserve flagged AI as a top systemic risk. Bain reckons the industry needs to find eight hundred billion dollars of annual revenue it doesn’t yet have. Worth watching.

Read those together and you get the geometry of the next year. Demand is real, capability is real, the capacity is sold out. This is not the dot-com fibre glut. The danger is the financing, and the first crack will show in a credit spread or a missed revenue number not utilisation rate or memory walls.

Where this goes, and where I’d stand

So, a 12 month prediction.

The base of the stack stays sold out and keeps raising prices. Claude puts that at about 85%, and the only thing that breaks it is a financing accident upstream. Nvidia’s share drifts to the low 70s rather than falling off a cliff, the moat holding longer than the bears want.

And power overtakes chips as the botteneck, and the headlines fill up with gigawatts and gas turbines and small reactors. And somewhere in the next year, I think more likely than not, one of the heavily indebted neoclouds or one of the circular-financing counterparties has a scare, a refinancing that won’t close or a number that comes in light, and the most leveraged names take a beating. A scare, I’d say, is the base case. A full 2000-style bust is not, maybe a one-in-four, and it needs a marquee counterparty to actually break, an OpenAI revenue miss or an Oracle that can’t roll its debt.

As for where I’d stand, note I am a seed-stage investor/hop hop aficionado not an economist, I can’t wait for the data, I have to bet before it. If the whole stack is renting from the fab, you want to own the fab, or the things the fab can’t operate without. In public markets that is TSMC, sold out with pricing power, and ASML, the purest chokepoint, and the memory makers if you’ve the stomach for the cycle. The contrarian version is the boring stuff nobody prices as “AI,”. e.g the materials and consumables that get used up on every wafer regardless of the logo. Can I interest anyone is a little photoresist?

But the best thesis is probably power. If you know, you know. The constraint moved to electrons faster than the companies that sell electrons re-rated. Gas turbines sold out to 2030, the grid and transformer names, the independent power producers and the nuclear restart stories. Won’t someone think of the climate tech funds? what will they do? when the future of compute becomes power infra?

The irony in all of it is that the thing most likely to break this is not whether the AI is any good. The AI is plenty good already. And people clearly want it. The thing most likely to break it is the daisy-chain of cheques being written to pay for the electricity to run it. The chips will keep coming out of Taiwan either way. The question is: who will still be standing to plug them in.

It’s all going to come back to Centrica isn’t it. I am going to have to buy Centrica…

To make the format even make a semblance of sense, here are 3 stories. Three Story Friday. This format is a bloody mess.

1. TPUs To Go

First up, Google. The Journal says they’re building a real chip business now, selling TPUs into other people’s data centres rather than just renting them out inside Google Cloud, and Sundar flagged as much on the Q1 call. The deals are real, too: Anthropic’s on the hook for up to a million Ironwood chips (that’s v7), over a gigawatt of them this year and heading to 3.5 by 2027, with 400k bought outright through Broadcom for 10 billi, and Meta’s supposedly in talks as well. Ironwood comes in at about 90% of a Blackwell for maybe 44% less per chip, so a real competitive part. If you want the technicals and the memes there’s always Dylan, otherwise you get Jay-Z quotes, and you will like it.

Here’s my unique take, as Opus called it. Google doesn’t actually make a TPU, and once you read the map, you know: Broadcom designs the core, MediaTek does the cheap inference one, and TSMC bakes the whole thing on 3nm. So Google “selling you a TPU” is really Google taking a cut on top of Broadcom’s design cut on top of TSMC’s wafer, and going merchant is just Google reaching for a bigger slice of that stack.

Source: CNBC.

2. Everything Must Go

And with Amazon, even more hands in the pie, as the old saying goes. They’re in talks to put Trainium in other companies’ data centres, which would be the first time they sell the chip instead of renting the compute. Trainium3 is their first 3nm part, about 4x Trainium2 at half a GPU’s price, and it’s the chip behind Anthropic’s Project Rainier, apparently nearly 1 million of them soon, + 5GWs of power + 100bn dollars committed to AWS.

Note, the design partner. Trainium2 was a Marvell job, for Trainium3 it’s Annapurna for the front-end now and Alchip for the back-end, so Marvell got dropped in a single generation. Brutal business. So yes, Amazon are selling "their chip”. But also, like not really. Hell of a value chain, you’ve got there. A Trainium on its own in someone else’s building is an ASIC with a worse software story than the GPU it’s meant to beat, and the cloud wrapped around it is the only reason it works at all. Does anyone outside the Anthropic mates’-rates actually buy that?

3. Reverse Ferret

So design is a brutal business. So if I am Intel, what do I do? I go into an even better business. Making chips. Like we used to do, but got out of it because margins were poor and it was soo expensive. Well times have changed.

Well, Intel just hired Seok-Hee Lee, ex-CEO of SK Hynix (the HBM maker mainly now), to run its foundry and packaging. Look at the map again. Intel, the original chip vendor is back in the manufacturing game. But this isn’t about margins and money. It’s an American hedge against Chinese invasion of Taiwan.

it’s becoming ever clearer what Intel is. Not AI chips. It’s under 1% of accelerators, killed the Gaudi target in October and canned Falcon Shores. It’s good at the unsexy stuff: the x86 base, being the only leading-edge fab on American soil with Trump holding 10%, 18A finally shipping in Panther Lake, and the one thing people actually like: packaging, EMIB and Foveros, where it’ll package a TSMC die and get paid even when it doesn’t do the wafer. The Lee hire is Intel betting the money’s in manufacturing, not the chip. This is what the chart says to do. It’s a good chart. That’s strategy.

The stock’s though? It’s up c.190% this year on a 78x forward multiple, so the market’s already paid for a comeback. It better show up. Foundry lost 10.3 billion last year, 18A is making margins worse before it makes them better, and there’s no committed leading-edge customer signed. But remember A is smaller than nm. So A is better than NM. It’s fewer letters for a start.

Long one today. Hope you made it. You are loved.

If you missed it:

Been a while, enjoyed it. You're a gem